Vishal Garg, Better Mortgage Founder and CEO, demystifies the low down payment mortgage.

Becoming a homeowner is a huge milestone in many people’s lives, but it can be hard to know when you’re ready. At Better Mortgage, we've found that many people don't take the next step because of how daunting it can seem to save up for a large down payment.

We want to help you see yourself as a homebuyer by giving you accurate, transparent information about your financing options. In addition to eliminating unfair commission structures, lender fees, and bait-and-switch quotes, we work with government-backed investors like Fannie Mae and other reputable banks to offer a variety of loan types, to help people chose the best financing option for them.

Considering a 3-5% down payment

For example, we can offer qualified borrowers financing options with as little as 3% down. Now, I know what you’re thinking. That sounds risky. But it’s not – anymore. Before the housing crisis, these types of loans were often offered to people who were at a high risk of defaulting, such as people with extremely high debt-to-income ratios. Since then, the mortgage industry has been regulated to protect people from those kinds of predatory loans.

For borrowers with great credit and a steady income, a 3-5% down loan can be a financially sound option, allowing you to start investing and building equity sooner.

The difference between what you can afford and the size of your down payment

Essentially, you pay for your home with:

- An initial large payment (your down payment)

- Ongoing installments, with interest (your monthly mortgage payment)

Many potential homeowners focus on the first part, which is their down payment. But lenders are also looking at your future ability to pay, which is indicated by a steady income and a great credit score.

Let’s look at an example

Let’s say you have high student loan debt, but a stable career with steady income (and the tax returns and pay stubs to prove it). And you live in a city where your monthly rent is high – even higher than what a monthly mortgage payment might be.

In this instance, you may not have a 20% down payment saved up, since most of your income has gone towards rent and paying off student loans. But your income profile, and the fact that you’re already making high rent payments, can be a signal to lenders that you’ll be able to make consistent mortgage payments.

The bigger picture: backed by data

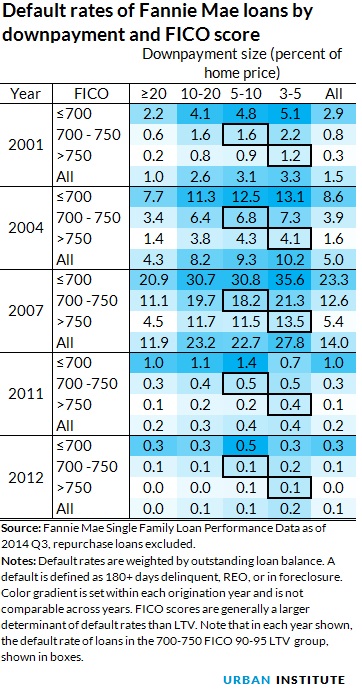

An analysis of historical loan data by Laurie Goodman, Jun Zhu, and Taz George at the Urban Institute shows why government-backed investors like Fannie Mae see relatively little risk in qualifying mortgage loans with down payments as low as 3-5%:

Data shows that credit is a stronger indicator of default risk than down payment size. The percentage of defaults of 5-10% down loans versus 3-5% down is very similar.*

“Of loans that originated in 2011 with a down payment between 3-5 percent, only 0.4 percent of borrowers have defaulted. For loans with slightly larger down payments – between 5-10 percent – the default rate was exactly the same. The story is similar for loans made in 2012, with 0.2 percent in the 3-5 percent down-payment group defaulting, versus 0.1 percent of loans in the 5-10 percent down-payment group.” – Urban Institute

What does this mean for Americans with goals of homeownership? For a couple with $25,000 saved up for a down payment, it could be the difference between being able to put 10% down for a 1-bedroom home that costs $250,000, versus putting 5% down and getting for a 2-bedroom home for $500,000.

The bottom line

We think if you’re considering homeownership, you shouldn’t have to keep renting just to save up for a large down payment. Government-backed investors like Fannie Mae agree. They want to help more people build equity through homeownership, and they’re doing so by backing loans with as low as even a 3% down payment, for borrowers who fit the profile.

If you’re considering buying a home, we’re here to help you understand your options. Take a few minutes today to explore whether homeownership is a possibility with our 3-minute basic pre-approval. There is no fee, no obligation, and researching your financial options will not affect your credit score. You can also talk through your options by scheduling a free call with one of our non-commissioned Mortgage Experts.

*Why the Government Sponsored Enterprises' support of low-down payment loans again is no big deal