Some homeowners get HELOC approval in just a few days, while others wait up to six weeks.

A home equity line of credit (HELOC) offers flexible access to your property's value, creating a revolving credit line you can tap into as needed during the draw period.

Your HELOC timeline depends on several factors: Your lender's efficiency, whether you have all the documents prepared, and the type of appraisal. Traditional banks often need two to four weeks, while online lenders like Better can reduce this timeframe.

How long does the HELOC process take?

Typical time frame: 7 days to 6 weeks.

A HELOC application can take anywhere from five days to six weeks. Traditional banks typically take two to six weeks. Online lenders have digitized the process and may deliver faster approvals.

Better can get your funds in as little as seven days².

Why timelines vary by lender and borrower readiness

Factors affecting how quickly you’ll access your HELOC funds include:

- The type of lender: Traditional banks use multi-step reviews. Online lenders like Better use tech-driven automation.

- The home appraisal method: In-person appraisals can take up to two weeks. AVMs (Automated Valuation Models) allow for instant valuation.

- The applicant's readiness: Turning in documents fast can cut processing time.

- The loan's details: Smaller loans (under $250K) may face fewer hurdles.

❓Not sure if a HELOC is right for you? Learn more about other ways to tap into your home’s equity via home equity loan or cash-out refinance.

What is the process to get a HELOC?

A home equity line of credit follows a path from application to funding. Understanding each step helps you access your funds sooner.

1. Measure your home equity

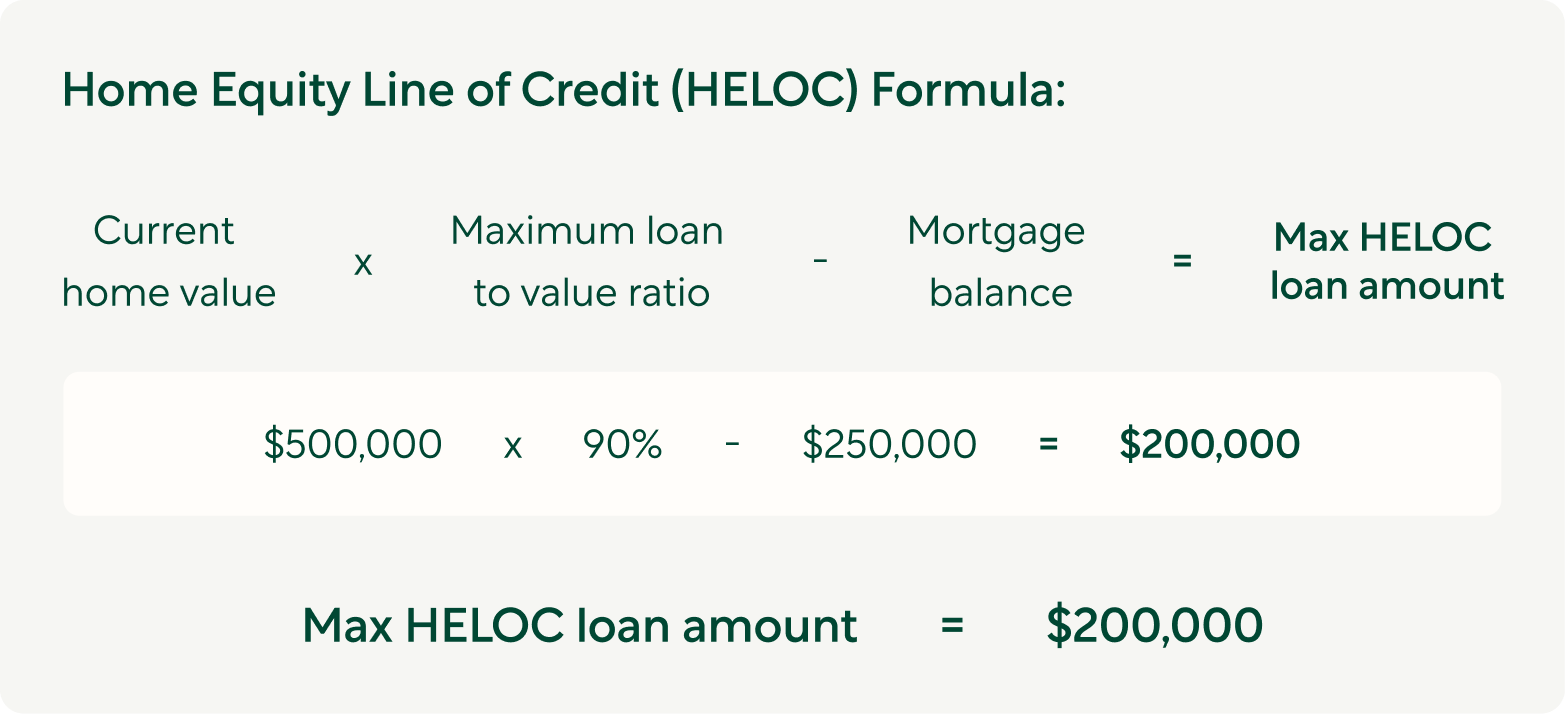

First, calculate your available equity which is the difference between your home's current value and your remaining mortgage balance.

Most lenders allow borrowing up to 80 to 85% of a home's value minus your mortgage balance. Better allows homeowners to borrow up to 90%³ of their home's value.

For example, if your home is worth $500,000 and you owe $250,000 on the mortgage, you have $250,000 in equity.

But you won't be able to access all of that cash. If the lender allows access up to 90 percent of this equity, your total mortgage debt can't surpass $450,000, which is 90 percent of the $500,000 home value.

$450,000 minus the $250,000 owed on the primary mortgage leaves $200,000 as the maximum size of the HELOC.

2. Research and compare lenders

Next, evaluate different lenders carefully. Online lenders can complete faster approvals and, sometimes, more competitive rates through digital processes than traditional banks. Traditional banks, on the other hand, can offer in-person customer service.

Compare interest rates, fees, repayment terms, and customer service reputation to find your best match.

With any lender, you'll need to qualify for the loan, which leads us to Step 3.

3. Gather documentation

Before applying, collect all necessary financial documents. Most lenders will ask for:

- W-2s / 1099s / tax returns

- Bank statements

- Mortgage statements

- Employment info

4. Submit your application

With documents in hand (or on screen), complete your application online. The lender will pull your credit report and verify your residence history, employment, and income information during this stage.

5. Underwriting and appraisal

After submission, the underwriting process begins. Your lender reviews your creditworthiness, debt-to-income ratio, and available home equity.

While this happens, a home appraisal finds the value of your home which is key to measuring home equity. Appraisals happen through an automated valuation model (AVM) or by a traditional in-person assessment.

6. Final approval and closing

Once underwriting completes, you'll receive final approval. The lender checks your home title to verify other loans you may have against the home. Finally, you'll sign loan documents, after which your funds become available.

How to speed up the HELOC process

The key to fast HELOC approval? A fast, digital lender combined with a responsive applicant.

Look for:

✅ Faster processing:

Online lenders with automated systems can approve HELOCs in less than a week, compared to traditional banks' two- to six-week timeframe. With Better's One Day HELOC, for example, you could get a decision in 24 hours ¹, cash in 7 days ²

✅ Electronic verification

Digital-first lenders connect directly to your financial accounts rather than requesting paper documents, saving lots of time.

Modern lenders using Automated Valuation Models (AVMs) skip the time-consuming traditional appraisal process. AVMs can generate a home value before a human appraiser can even be scheduled for an in-person visit.

Be prompt with document submission and communication

Your responsiveness directly impacts how quickly you'll get approved.

To speed up your application:

- Submit all requested documentation immediately

- Answer lender questions the same day they're asked

- Review and sign disclosures without delay

- Make yourself available for appraisal scheduling (if applicable)

Nearly every mortgage professional highlights this point: Borrower delays account for a significant portion of extended timelines.

Understand your credit and debt-to-income ration

Checking your own credit score and calculating your debt-to-income ratio (DTI) before applying helps prevent unexpected roadblocks.

Better's HELOC requires a minimum credit score of 640 and a maximum debt-to-income ratio of about 50%.

To check your own DTI, add up all your monthly loan payments and credit card minimum payments. Then divide this total by your gross month income. Multiply the answer by 100. Be sure to include the new HELOC payment into your total monthly debt payments.

Have documents ready for DTI calculation

Organize these documents before applying:

- Recent pay stubs and tax returns

- Current mortgage statements

- Proof of homeownership

- Bank and investment account statements

This prep work creates a smooth application process from the start, eliminating back-and-forth requests that delay processing.

Common delays and how to avoid them

Even with careful planning, HELOC applications can hit snags that extend your waiting time from days to weeks. To speed your application, pay attention to:

Missing or incomplete documents

Documentation issues remain a primary cause of HELOC processing delays.

To prevent documentation delays:

- Create a checklist of required documents before applying

- Submit all requested materials in your initial application

- Keep recent pay stubs, tax returns, and bank statements easily accessible

- Double-check information for accuracy before submission

Slow appraisal scheduling

Home appraisals often become bottlenecks in the HELOC process. Traditional in-person appraisals require scheduling, property visits, and detailed reports, activities that may take a couple weeks depending on appraiser availability.

To speed up the appraisal, ask your lender about using an AVM. If you have more equity than you plan to borrow, the lender may agree.

Slow response to questions from lender

Delays occur when either party fails to respond promptly. Questions remain unanswered and critical decisions await approval.

To maintain efficient communication:

- Check email (including spam folders) daily

- Return calls from your lender immediately

- Set up alerts for lender messages

- Designate a specific contact person with your lender

- Review and sign disclosure documents promptly

When working with Better, you'll have a borrower portal that allows you understand clearly where you are in the process and contact your loan officer directly.

Your time matters: Work with a fast HELOC lender

Getting a HELOC doesn't have to feel like watching paint dry. While traditional banks may need a month to six weeks to process your application, digital lenders can cut this timeline to just days. Your own readiness, having documents organized and responding quickly, plays a huge role in how fast you'll access your home's equity.

Though the average HELOC takes about 30 days to approve, you can significantly shorten this timeline by applying our acceleration strategies.

Better stands out in the industry with their One Day HELOC™ decision process and funding in as little as seven days, proof that the right lender makes all the difference.

...in as little as 3 minutes – no credit impact

Disclaimers

¹ One Day HELOC offers customers who provide required financial documentation within 4 hours of rate lock the opportunity to receive an underwriting determination (additional requirements may apply) within 24 hours of rate lock. Initial approval does not guarantee final underwriting approval. See One Day HELOC Terms and Conditions. Assumes borrowers are eligible for the Automated Valuation Model (AVM) to calculate their home value, their loan amount is less than $400,000, all required documents are uploaded to their Better Mortgage online account within 24 hours of application, closing is scheduled for the earliest available date and time, and a notary is readily available. Funding timelines may vary and may be longer if an is required to calculate a borrower’s home value.

² Assumes borrowers are eligible for AVM to calculate their home value, their loan amount is less than $400,000, and all required documents are uploaded to their Better Mortgage online account within 24 hours of application. Closing timelines may vary.

³ $50,000-$500,000 loan amount at up to 90% of your property’s value. Maximum LTV dependent on borrower eligibility.